FROM PAYCHECK TO PORTFOLIO

Financial Literacy for the First-Time Employee — How to Turn Your First Check Into Your First Strategy

A Real Ones In The Room / THE W.E.A.L.T.H. LAB Installment for Students, First-Time Employees, Parents, Employers, Educators, and Every Leader Who Claims They Want the Next Generation to Win

Before you read another word, ask yourself these three questions:

1. If young people are finally being taught how to earn, why are we not teaching them how to keep, grow, protect, and multiply what they earn?

2. If the first job introduces students to labor, wages, taxes, banking, spending, pressure, and responsibility, why would we separate employment readiness from financial literacy?

3. If trading, investing, credit, budgeting, taxes, entrepreneurship, and ownership are all part of how money moves, why are students still being handed fragments instead of the full blueprint?

Quote to carry:

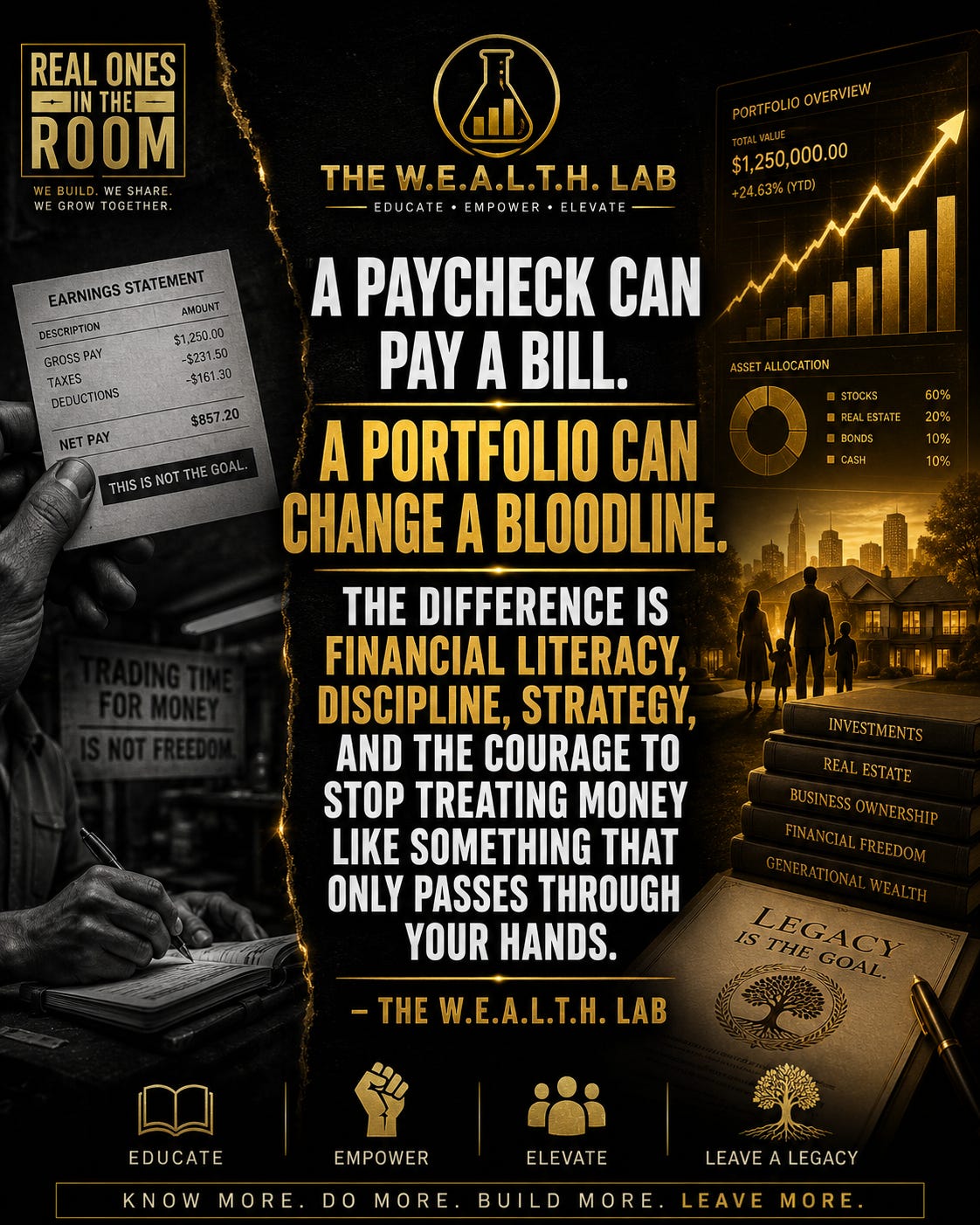

“A paycheck can pay a bill. A portfolio can change a bloodline. The difference is financial literacy, discipline, strategy, and the courage to stop treating money like something that only passes through your hands.” – THE W.E.A.L.T.H. LAB

THE LAB IS OPEN. Let’s Tell the Truth.

Your first paycheck is not just money. It is evidence. Evidence that your time has value, your labor has power, your name can enter a payroll system. Evidence that effort becomes income, income becomes savings, savings becomes investment, investment becomes ownership, ownership becomes leverage, and leverage becomes freedom. But only if somebody teaches you what to do after the money hits.

Because if nobody teaches you, the economy already has plans for your paycheck. The phone company has a plan. The sneaker store has a plan. The food delivery app, the streaming service, the credit card company, the car note, the landlord, the tax system, the algorithm, the mall, the “buy now, pay later” industry — everybody has a plan for your money. The question is: do you?

We already handled how to get the job. This is the next level. This is the moment where the student becomes the employee, the employee becomes the money manager, the money manager becomes the investor, the investor becomes the strategist, and the strategist begins building the foundation of a portfolio. From paycheck to portfolio. From survival to strategy. From labor to leverage. From financial confusion to financial command.

And yes — trading belongs in this conversation. Not reckless trading, not gambling, not hype, not fake screenshots, not emotional clicking. We’re talking about trading as a disciplined financial literacy laboratory: a place where students learn risk, probability, patience, data, psychology, structure, journaling, position sizing, and respect for capital. Trading is not the whole conversation, but taught correctly, it becomes one of the most powerful classrooms inside it. Because markets expose your habits, your emotions, your discipline, and your patience. Financial literacy is not just knowing vocabulary — it’s knowing how to behave around money.

THE RECEIPTS: Why This Matters Right Now

Young people are already in the economy. In July 2025, the Bureau of Labor Statistics reported 21.1 million employed youth ages 16–24 in the U.S.; 25% worked in leisure and hospitality, 17% in retail trade, 14% in education and health services. Those are first-job industries, real-world money classrooms. The youth unemployment rate for that group was 10.8%, higher than the year before — meaning the first-time employee isn’t walking into an easy game. They’re entering competition, rejection, and a market that demands preparation.

Financial pressure isn’t theoretical. The Federal Reserve’s 2025 household well-being report found only 63% of adults could cover a $400 emergency expense cleanly. FINRA’s National Financial Capability Study shows financial capability is lower among young adults, people of color, and lower-income households. And New York? The state’s personal finance education mandate kicks in for the 2026–2027 school year. This isn’t “someday.” This is mandate season. The job market is real. The paycheck is real. The pressure is real. The gap is real. The opportunity is real. And THE LAB is open.

PART ONE: Your First Paycheck Is a Test

The first mistake young workers make is thinking the first paycheck is only for spending. No. The first paycheck is a test. It tests whether you understand delay, priorities, taxes, gross versus net pay, needs versus wants, and whether money without a plan disappears. It tests whether you can separate temporary excitement from long-term strategy.

That first check feels good. It should. You earned it. You showed up, dealt with customers, listened to managers, handled the schedule, moved your body, used your time. Pride is earned. But pride without a plan becomes spending. Spending without a plan becomes regret. So before the check hits, the student needs a system. Not a speech. A system.

PART TWO: Gross Is Not Net — The Paycheck Breakdown

If you work 20 hours at $16 an hour, you might think: $320. But that’s not your pocket money. Taxes come out. Deductions happen. Uniforms, transportation, food, phone costs — all of it nibbles at what remains. Your hourly wage is not your lifestyle. Your gross pay is not your spending money. Your net pay is not all free money. Your first check is the beginning of your first money plan. Understand the system, and you stop being shocked by the receipt.

PART THREE: The First Check Formula

Every first-time employee needs a simple formula — not Wall Street language, not a 90-page spreadsheet.

THE LAB First Check Formula:

1. Give every dollar a job before you spend.

2. Pay your future first — even a tiny saving counts.

3. Separate needs from wants: food and transport vs. impulse.

4. Build emergency money before flex money.

5. Learn before you invest — don’t touch what you don’t understand.

6. Track every dollar for the first 90 days — you can’t manage what you refuse to measure.

7. Protect your name — your financial reputation starts now.

Start there. Build from there. Master from there.

PART FOUR: The First 90 Days — Employee to Money Manager

The first 90 days aren’t just about proving yourself to the employer; they’re about proving yourself to yourself.

Days 1–30: Awareness

Learn your schedule, pay cycle, net pay, transport costs, what you spend on food and impulse. Open or confirm your bank account. Read your pay stub. Save something from every check. Don’t try to look rich. Learn how money moves.

Days 31–60: Control

Create a simple budget. Build a small emergency cushion. Limit impulse purchases. Learn about credit, direct deposit, debit vs. credit, overdraft fees. Start building discipline.

Days 61–90: Strategy

Set a savings goal. Study investing basics — risk, compound growth, what trading is and isn’t. Start paper trading only if learning. Journal your financial decisions. Connect the job to a future plan.

By day 90, you shouldn’t just be an employee — you should be a young financial operator. Not perfect. But awake.

PART FIVE: Banking Is Access, Not Just Basics

A young person’s bank account is their first formal financial tool. But banking must be taught: checking vs. savings, direct deposit, overdraft fees, debit cards, minimum balances, fraud, scams, mobile deposits, what happens if you lose your card or share your info. Banking is where the young worker learns financial boundaries. And boundaries matter — protecting your account is the start of protecting your credit, identity, and future.

PART SIX: Credit Is Reputation, Not Free Money

Say it with force: Credit is not free money. Not a flex. Not a toy. Credit is reputation, access, trust on paper, a financial résumé. It can help you rent an apartment, affect insurance, car financing, business funding, interest rates. It can also become a trap if you don’t understand it. That’s why Leverage Credit Recovery belongs in this conversation.

The rules: Don’t borrow to impress people not paying your bills. Don’t use credit to build an image before you build income. If you can’t explain the interest rate, payment date, minimum payment, late fee, and payoff plan, you’re not ready to swipe. Credit can be a weapon — but only if you’re trained. Untrained credit becomes a weapon pointed back at you.

PART SEVEN: Budgeting Is Permission with a Plan

Budgeting isn’t “I can’t have fun.” It’s deciding what fun you can afford without sabotaging your future. A budget tells your money: this goes to transport, food, savings, phone, family support, emergency money, planned fun. This does not go to impulse foolishness. The problem isn’t spending; it’s unconscious spending. The problem isn’t buying sneakers; it’s buying sneakers while your account gasps for air. Real Ones don’t shame young people for wanting nice things — we teach them how to afford nice things without becoming owned by them.

PART EIGHT: Emergency Money Is Your First Defense

Before portfolio, emergency fund. Before flex, cushion. The Fed’s 2025 report showed only 63% of adults could handle a $400 emergency cleanly. A young worker with even $100 saved has more breathing room than zero. $250? More options. $500? More confidence. $1,000? A foundation. That’s how the portfolio begins — not with hype, but with a cushion.

PART NINE: Investing — Ownership Begins with Understanding

Investing isn’t just for rich people or Wall Street. It’s how ordinary people participate in ownership. But students need to know: stocks, bonds, index funds, ETFs, retirement accounts, compound growth, diversification, risk, volatility, dividends, brokerage accounts, the difference between investing and trading, ownership and speculation, patience and gambling. Long-term investing is ownership over time. Trading is planned execution around market movement. Both require discipline, education, risk management, emotional control. Confusing them is how people get hurt.

PART TEN: Trading Is the Great Equalizer — When Taught with Discipline

Trading can be a great equalizer because charts don’t ask where you live, what your parents make, your zip code, or your popularity. The market responds to structure, liquidity, timing, risk, psychology, patience, discipline, execution. That’s powerful.

But let’s not lie: trading is dangerous when taught wrong. It humbles you fast. It exposes greed, impatience, revenge behavior, overconfidence, lack of preparation. That’s why THE LAB doesn’t teach trading as a fantasy — we teach it as a discipline. A trader must learn accumulation, demand, distribution, supply, support, resistance, break of structure, change of character, trend, volume, liquidity, risk-to-reward, position sizing, stop losses, journaling, timeframes, emotional discipline, patience, confidence without cockiness. And above all: do not risk money you cannot afford to lose. Trading is not rent money, lunch money, emergency money, borrowed money, desperation money. It is skill money, education money, practice money, planned risk money. That distinction can save a young person from disaster.

PART ELEVEN: THE LAB Zone Strategy — Structure Over Chaos

Markets move through zones. Pressure builds. Buyers defend. Sellers reject. A student who learns zones isn’t just learning trading — they’re learning to read behavior. That’s the deeper lesson.

· Accumulation: Smart money may be building positions. The chart looks boring, but preparation is happening.

· Demand: Buyers show interest. Value is recognized.

· Distribution: Strength may be sold into excitement. Don’t confuse attention with opportunity.

· Supply: Sellers take control. Resistance is information.

· Support: A floor where buyers defend. Know what holds you up.

· Resistance: A ceiling where sellers push back. Every barrier must be respected.

· Break of Structure: A possible shift in trend. When structure breaks, adjust.

· Change of Character: The market behaves differently. When behavior changes, pay attention.

This is why trading belongs inside financial literacy — it teaches pattern recognition, risk, patience, decision-making under pressure, and that preparation matters before execution.

PART TWELVE: The 1-Hour, 15-Minute, 5-Minute Plan

THE LAB’s timeframe structure is about discipline, not random clicking.

· 1-Hour Chart: The Map — Identify larger structure, trend, major zones, liquidity, the broader story. Teaches patience: “Understand the battlefield.”

· 15-Minute Chart: The Setup — Refine the idea. Is price approaching a zone? Is momentum shifting? Teaches selection: “Not every movement is your trade.”

· 5-Minute Chart: The Execution — Entry trigger, stop, target, risk, invalidation. Teaches precision: “If you enter, enter with a plan.”

This is bigger than trading. This is life: map, setup, execution. Vision, strategy, action. That’s THE LAB.

PART THIRTEEN: Moving Averages — 9, 21, 100 as a Second Strategy

Moving averages help students see trend and momentum visually.

· 9 MA: Short-term momentum, fast, sensitive.

· 21 MA: Intermediate trend, rhythm identifier.

· 100 MA: Larger structure, dynamic support/resistance.

Moving averages are tools, not magic. Tools require rules, rules require discipline, discipline requires journaling, journaling requires honesty, honesty requires maturity. Trading isn’t just financial education — it’s character education.

PART FOURTEEN: Risk Management — The Line Between Trader and Gambler

The 1% rule is survival: risk no more than 1% of your account per trade. $1,000 account? Risk $10. Not $100, not “I’m sure this one will hit.” The goal is to stay in the game long enough to master the skill. Position sizing formula: Risk Amount ÷ Stop Loss Distance. Know your risk, exit, invalidation, and target before you enter. Don’t move the stop out of fear. Don’t increase size out of excitement. Don’t revenge trade. Trading forces the student to ask: How much can I lose? What’s my plan? What’s my evidence? What’s my emotional state? That’s elite education.

PART FIFTEEN: The Trading Journal — Where the Real Education Happens

The trade isn’t complete when you exit; it’s complete when you review. Track: date, market, timeframe, setup, zone, entry, stop loss, target, risk, position size, result, screenshot, emotion before/during/after, mistakes, rules followed, lessons learned. A trading journal is a mirror. Real Ones don’t run from the mirror — they use it.

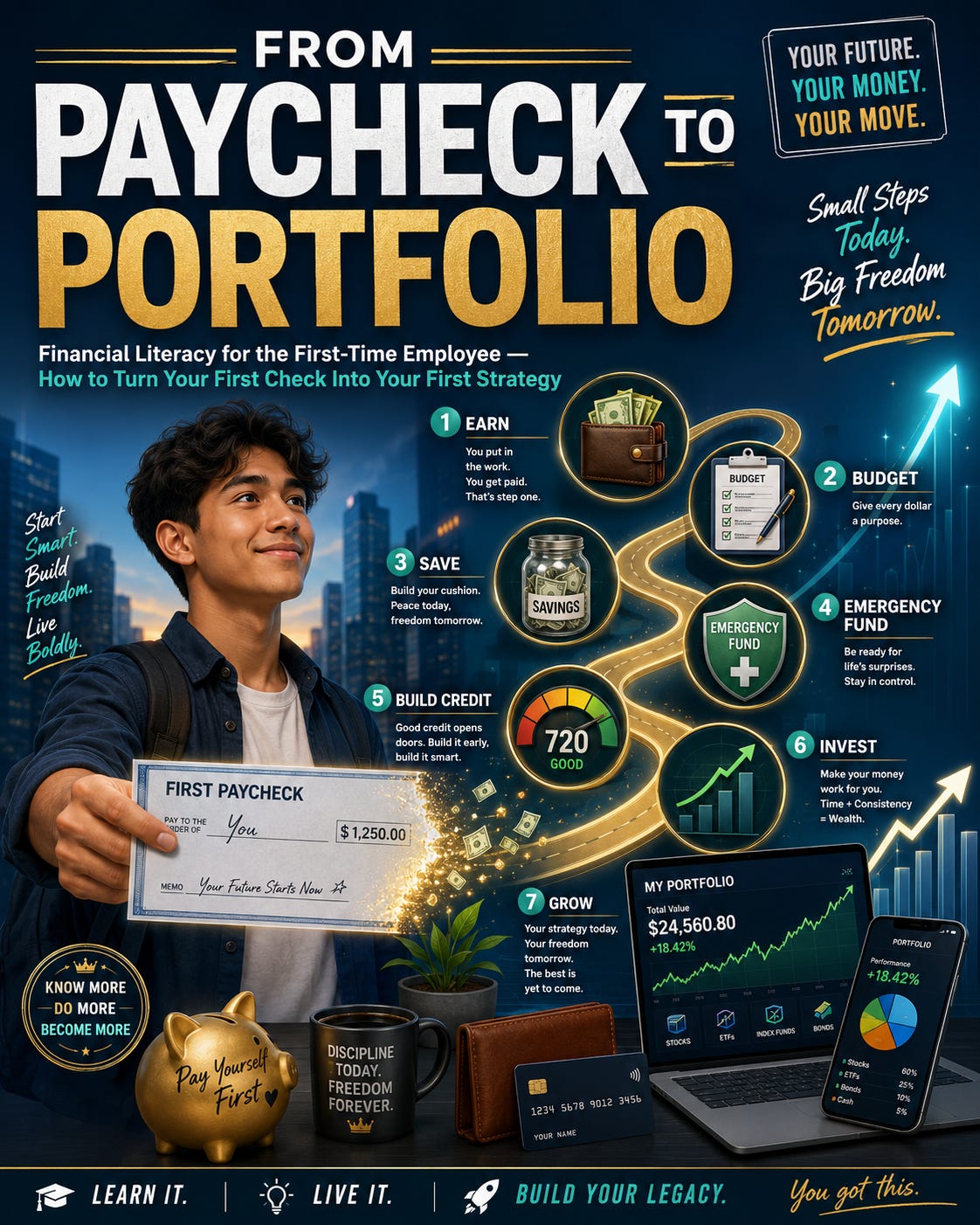

PART SIXTEEN: Paycheck to Portfolio — The Real Sequence

The first-time employee doesn’t jump from first paycheck to trading account. The sequence matters:

1. Earn – Get the job, show up, build work ethic.

2. Track – Know income, expenses, pay schedule.

3. Save – Build emergency money, create a cushion.

4. Bank – Use direct deposit, avoid fees, protect your account.

5. Budget – Plan needs, wants, savings, giving, growth.

6. Credit – Learn before borrowing, protect your score.

7. Invest – Study long-term ownership, start small, stay consistent.

8. Trade Education – Paper trade first, study charts, journal everything.

9. Portfolio – Build a balanced financial life: emergency fund, banking, credit, investments, skills, income streams, career growth.

That’s the blueprint. Not paycheck to panic — paycheck to portfolio.

PART SEVENTEEN: The Portfolio Is Bigger Than Stocks

Your real portfolio includes skills, work experience, references, savings, banking relationship, credit profile, investment knowledge, trading journal, professional network, resumé, certifications, business ideas, transportation plan, digital reputation, communication skills, discipline, confidence, character. Assets aren’t just things you buy — they’re things you build. Your skill is an asset. Your name is an asset. Your ability to manage risk is an asset. THE LAB teaches the whole person how to become harder to exploit.

PART EIGHTEEN: The Employer’s Role — Paychecks Are Not Enough

Employers, don’t just hire students — educate them. A paycheck without development is incomplete. If a young person’s first job is with you, you’re shaping their relationship with work, leadership, professionalism. Offer pay stub education, direct deposit guidance, schedule literacy, workplace rights, professional communication, savings challenges, mock interviews, career pathway maps, financial literacy workshops. This isn’t charity — it’s workforce development, talent pipeline, community investment. Stop waiting for polished talent while refusing to polish talent.

PART NINETEEN: The School’s Role — Stop Teaching Money Like It’s Abstract

Financial literacy cannot be dry worksheets with fake numbers. It must include paychecks, taxes, W-4s, budgeting, banking, credit, debt, rent, inflation, insurance, investing, trading literacy, scams, contracts, consumer rights, entrepreneurship. New York’s mandate creates the opening. Will districts treat it like compliance or transformation? Yonkers can lead. New York can scale. America can learn. But only if adults stop shrinking the assignment.

PART TWENTY: Parents and Caregivers — The Household Needs the Playbook

Many households were never taught this. THE LAB isn’t here to shame — we’re here to equip. Parents and caregivers can help by asking: Did you read your pay stub? How much did you save? What did transportation cost? Do you understand your bank account? Are you learning before investing? This is how the home becomes part of the financial literacy ecosystem — not by knowing everything, but by refusing to stay disconnected.

PART TWENTY-ONE: The First-Time Employee Money Commandments

1. Thou shalt not spend the whole check.

2. Thou shalt read the pay stub.

3. Thou shalt know gross from net.

4. Thou shalt save before flexing.

5. Thou shalt not borrow to impress.

6. Thou shalt learn credit before using credit.

7. Thou shalt build emergency money.

8. Thou shalt invest only after understanding risk.

9. Thou shalt trade only with rules — no plan, no trade.

10. Thou shalt journal everything.

11. Thou shalt protect your name.

12. Thou shalt move from paycheck to portfolio.

PART TWENTY-TWO: What Trading Teaches That School Often Doesn’t

Patience. Emotional control. Risk management. Probability. Pattern recognition. Math. Journaling. Accountability. Data analysis. Decision-making. Self-awareness. Humility. A student can be academically gifted and financially reckless. Trading, when taught responsibly, forces the student to confront the relationship between decision and consequence. THE LAB isn’t creating hype traders — we’re creating financially literate decision-makers who understand money under pressure.

PART TWENTY-THREE: What Trading Is NOT

Not guaranteed income. Not a replacement for education or a job. Not a shortcut around discipline. Not a reason to ignore savings. Not something you do because you’re bored or because a stranger posted screenshots. Not with rent money, family money, or without a stop loss. Not without journaling, rules, or accepting losses. Any serious trading education must include risk warnings, practice, structure, and accountability. This article is educational, not individualized financial advice.

PART TWENTY-FOUR: The First-Time Employee Portfolio Plan

· Paycheck One: Read pay stub, save something, track every dollar, set up direct deposit.

· Paychecks Two–Four: Starter emergency fund, simple budget, learn credit basics, avoid unnecessary debt.

· Month Two: Study investing terms, compound growth, index funds, what trading is/isn’t, start paper trading journal.

· Month Three: Review spending, increase savings, create financial goals, practice trading only in simulation.

· Months Four–Six: Stronger emergency savings, explore long-term investing, build résumé value.

· Months Six–Twelve: Protect credit, explore investing with guidance if appropriate, keep trading education structured, build portfolio of skills and knowledge.

Structured. Not random. Not reckless. Not emotional.

PART TWENTY-FIVE: From Consumer to Owner

The economy trains young people to be consumers first. Buy this. Wear this. Subscribe to this. Prove yourself with this. THE LAB says no. We’re training young people to become owners. Own your time, paycheck, choices, name, skills, data, discipline, future. Own assets and equity where possible. A consumer asks, “What can I buy?” An owner asks, “What can I build?” A consumer spends for approval. An owner invests for leverage. That’s the shift. Paycheck to portfolio.

PART TWENTY-SIX: The Real Ones Call to Business, Banking, and Industry

· Banks/Credit Unions: Teach banking, credit, fraud prevention. Sponsor workshops.

· Employers: Don’t just hire — develop.

· Schools: Don’t just comply — transform.

· Elected Officials: Fund implementation, not just announcements.

· Philanthropists: Invest in infrastructure, not just praise.

· Traders/Educators: Don’t sell dreams — teach risk.

· Parents: Start the conversation now.

· Students: Don’t wait for perfect conditions. Begin.

PART TWENTY-SEVEN: Why THE W.E.A.L.T.H. LAB Is Built for This Moment

Because we understand the connected pathways. Day trading, retail, hospitality, fashion, fast food, travel, credit, employment, entrepreneurship, education, financial literacy. A student in retail learns inventory, sales, customer service, branding. In hospitality: service, patience, professionalism. In fast food: speed, systems, operations. In travel: logistics, global awareness. In trading: risk, psychology, discipline. In credit: reputation, access. In entrepreneurship: ownership, value creation. THE LAB doesn’t teach financial literacy as isolated vocabulary — we teach it as life infrastructure.

PART TWENTY-EIGHT: The Article They Should Have Given You Before the First Check

Before you spend, pause. Before you swipe, think. Before you trade, study. Before you invest, learn. Before you borrow, calculate. Before you flex, save. Before you panic, review the plan. Your first paycheck isn’t small. Your first budget isn’t small. Your first savings deposit isn’t small. Your first financial mistake isn’t final. Your first win isn’t luck if you built the system. This is the beginning.

FINAL WORD: We Are Not Teaching Young People to Chase Money — We Are Teaching Them Not to Be Chased by Poverty.

We’re not teaching greed — we’re teaching protection. Not arrogance — confidence. Not shortcuts — systems. Not gambling — risk management. Not flexing — ownership. Not how to become employees only — how employment becomes the first step toward economic power. The first job is not just a job. The first portfolio is the young person becoming aware of their own value.

That’s why we teach. That’s why we build. That’s why THE LAB is open. The poor, the working poor, the working homeless, the ever-eroding middle class, youth of color, students of all ages and backgrounds have been told too long to survive systems they were never taught to understand.

No more.

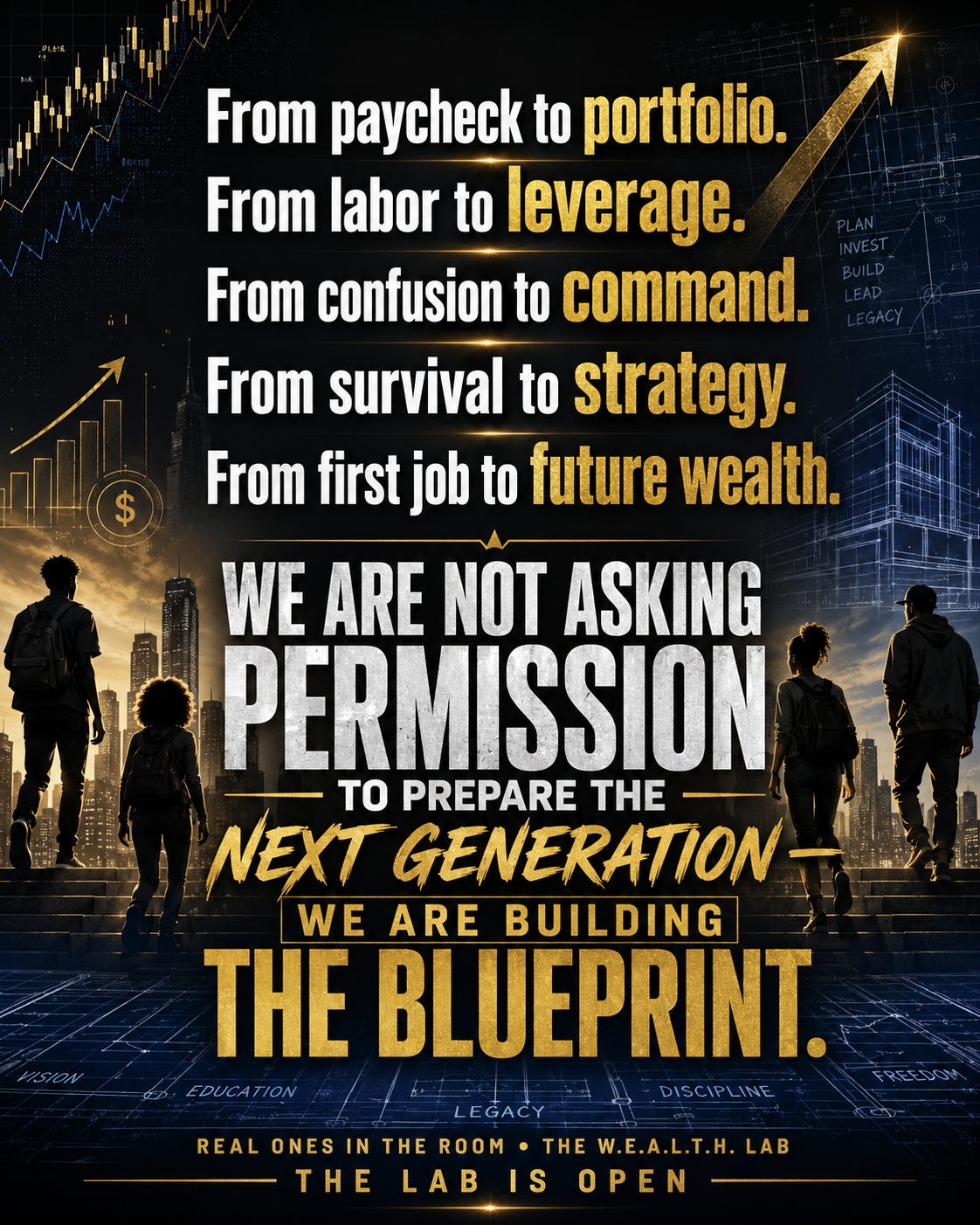

From paycheck to portfolio. From labor to leverage. From confusion to command. From survival to strategy. From first job to future wealth. We are not asking permission to prepare the next generation — we are building the blueprint.

Quote to build on:

“The paycheck proves you can earn. The budget proves you can control. The savings proves you can delay. The credit proves you can protect your name. The investment proves you can own. The trading journal proves you can discipline your mind. The portfolio proves you were never just working — you were building.” – THE W.E.A.L.T.H. LAB

Final Three Questions to Carry Forward:

1. If every paycheck is an opportunity to teach budgeting, banking, saving, credit, investing, trading discipline, and ownership, why would any school, employer, bank, or leader treat student employment like cheap labor instead of economic development?

2. If New York is entering mandate season, will Yonkers lead with a real financial literacy infrastructure — or will we settle for compliance when transformation is available?

3. When this generation asks whether we taught them how to earn, keep, grow, protect, trade responsibly, invest wisely, and build ownership, will we have receipts — or excuses?

Real Ones In The Room, THE W.E.A.L.T.H. LAB (THE LAB), Leverage Credit Recovery, and Yonkers Young Entrepreneurs — setting the standard, building the bridge, and ensuring the next generation has the tools to thrive, succeed, and prosper. Stay tuned for the next installment. The LAB is always open.

Best advice one could have, and you'll never regret it either.